This article describes a way to do payroll direct deposit with bitcoin. Using Strike, it seems the fees are very cheap (mostly zero) and the dollar-to-bitcoin conversions seem to be at very normal rates.

Before we get into the details of how to make “payroll direct deposit” work, it is perhaps helpful to remind ourselves of what happens generally if we have a goal of starting with USD and exchanging it for bitcoin and then transferring it to our hardware (cold) wallet for self-custody. Each of the following might happen:

- A starting point is that somehow we need to get our USD into the hands of an “exchange”. This might incur a credit card processing fee, or an ACH fee, or a bank wire fee.

- Once the USD is in the hands of the exchange, we need to click around and find out what exchange rate is going to be offered for the conversion of USD to bitcoin. Maybe we want to allow some time to pass, before doing the conversion, because we think the exchange rate will be more favorable at some future time.

- Some exchanges hide the transaction fee by tucking it into a less-favorable exchange rate. So there is no choice but to pay attention to the actual exchange rate that the exchange is going to use, which might be less favorable than some exchange rate charged by some other exchange. It might be less favorable than the published exchange rate that you see on some public web site.

- Assuming that we click the button to do the conversion to bitcoin, we may incur a transaction fee imposed by the exchange.

- Okay, so now we have some bitcoin. That’s great, but most people who have thought about it have the view that one ought not to hold any significant amount of bitcoin at an exchange. The exchange might get hacked, it might go out of business, or some KYC or AML trigger might tie up the bitcoin at an unpredictable time. The view is that in general any bitcoin that is in an exchange ought to get transferred to a self-custody cold hardware wallet. This means that barring some surprise, a fee will be incurred for the transfer of the bitcoin from the exchange to the cold wallet.

If you were to click around to look at various Internet discussion groups, you would find plenty of places where people describe their experiences with various cryptocurrency exchanges, with disappointingly bad exchange rates, disappointingly large fees for the conversion process, and disappointingly large fees for the “transfer out” to a cold wallet. You will see such reports for nearly all of the well-known crypto exchanges.

One approach for investing in bitcoin is “dollar cost averaging” or DCA (Wikipedia article). The term was coined by Benjamin Graham in his 1949 book The Intelligent Investor. Graham writes that dollar cost averaging

means simply that the practitioner invests in common stocks the same number of dollars each month or each quarter. (The same nomenclature applies to commodity markets, even gold). In this way one buys more shares when the market is low than when it is high, and he is likely to end up with a satisfactory overall price for all their holdings.

One way to do DCA would be via payroll direct deposit or recurring fixed-amount transfers to a retirement plan.

Which brings me around to the main point of this article. I have recently been using Strike as a way to handle payroll direct deposit with bitcoin. Using Strike, it seems the fees are very cheap (mostly zero) and the dollar-to-bitcoin conversions seem to be a very good rates. For one recent payroll, it looks like Strike gave me about 10% more bitcoin for my money than I would have gotten anywhere else. I will discuss this in some detail. Let’s talk through the various steps in a sequence.

Getting our USD into the hands of an “exchange”. Most payroll systems make it easy for the employer to honor an employee’s wish to carry out the direct deposits into two or more destinations. What I did recently was add a second destination, namely Strike, for a small portion of each of my paychecks. For the employee, such direct deposits usually incur no fee because the financial institutions are very glad to make the transactions free of charge. For the employer, typically the fee cost of direct deposits (in terms of fees charged by the payroll service provider) is small or zero.

Using an exchange rate to hide a fee. As I discussed above, some exchanges hide the transaction fee by tucking it into a less-favorable exchange rate. As far as I can see, in each of the currency conversions that Strike did for me, the exchange rate was quote normal. I will discuss this below.

Waiving transaction fee for a payroll direct deposit. Although Strike does charge non-negligible fees for currency conversion, Strike has an interesting policy for payroll direct deposits — it says it does not charge any fee for conversions of those amounts.

Transfer fee of zero. Strike’s transfer fees (for transferring bitcoin to a cold wallet) are the usual three amounts — a high amount for a fast transfer, a middle amount, or a low fee if you do not care how long it takes. But the low fee quoted by Strike for an outbound on-chain transaction is … wait for it … zero. Yes, if you pick the “zero” fee, you will have to wait a very long time for the transfer to finish. It will not show up in the mempool for many hours — often it will take half a day to show up in the mempool. (This means that in your cold wallet, you do not even see it as “pending” until many hours have passed.) I think the explanation for this is that if you pick the “zero” fee, Strike accumulates dozens of transactions and submits them to the mempool as a “batch”. The fee paid in the batch is thus benefiting all of the dozens of the transactions in the batch. Saying this differently, we can think of the transfer fee as being spread out over some dozens of transactions. In one zero-fee transfer from Strike to my cold wallet, the block explorer revealed that Strike had actually paid 14 cents (despite charging me nothing). But this was a batch of a dozen or so transactions, and maybe Strike just chose to absorb the 14-cent cost as part of serving a dozen of Strike’s customers.

The exchange rate. With an everyday purchase of bitcoin, the user may choose to click around and find out what exchange rate is going to be offered for the conversion of USD to bitcoin. The user might decide to allow some time to pass, before doing the conversion, because the user thinks the exchange rate might be more favorable at some future time. (By this we mean that the price of bitcoin might go down — so a particular number of USD would buy a larger amount of bitcoin.)

But with a payroll direct deposit, very likely the user will choose to check a box in the exchange’s system to authorize converting the USD to bitcoin pretty much instantly. What this means, in plain language, is that the user is choosing to trust that the exchange will not (for example) gouge the user by pretending that the exchange rate was higher than it really was. Or gouge the user by just making up an unfavorable exchange rate and hoping the user would not notice or would not go to the trouble to check it.

With all of this in mind, I decided to look at several of my recent payroll direct deposits that went to Strike. What I did was to look at the number of USD that reached Strike in each of the direct deposits. And I looked to see what amount of bitcoin I received in each of the currency conversions. I kept track of the date upon which each currency conversion happened (namely the date of the payroll direct deposit). And I divided the number of USD into the number of bitcoin to work out the effective exchange rate that Strike used on each payday.

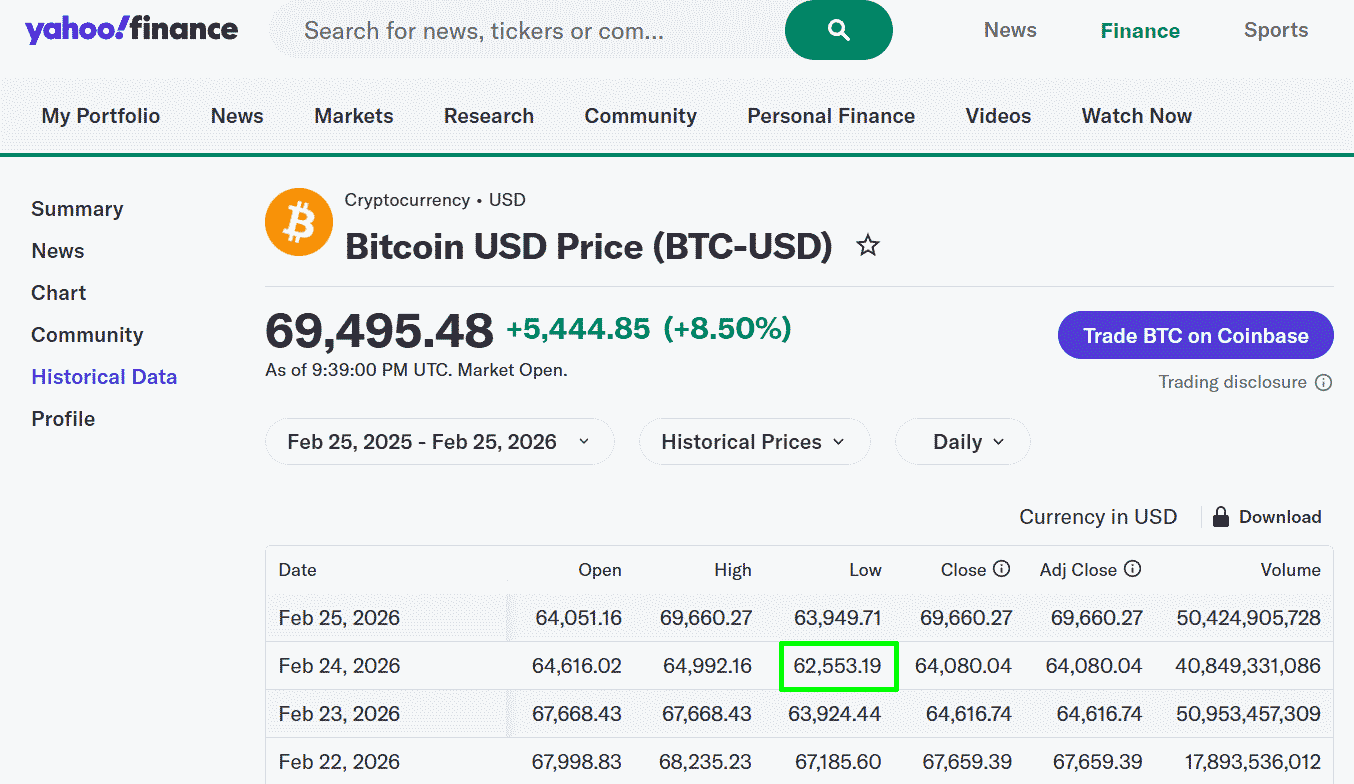

I then went to a very helpful web page from Yahoo Finance. It has a table with rows and columns. Each row is a particular date, starting with yesterday and the day before that, and so on. One column tells us what the opening price for bitcoin was that day and the closing price for that day (neither of which means anything for bitcoin since every exchange operates 24×7). It tells us the high for the day and the low for the day. Those two numbers do mean something.

| date | daily low exchange rate |

daily high exchange rate |

Strike exchange rate |

| February 24, 2026 | $62,553.19 | $64,992.16 | $63,208.55 |

| February 11, 2026 | $67,913.09 | $70,464.27 | $68,940.11 |

| January 28, 2026 | $87,228.92 | $89,427.13 | $88,245.66 |

| January 14, 2026 | $90,941.93 | $96,011.63 | $91,885.64 |

As we can see, on every one of the conversion dates, the rate that Strike used was within the range of reported exchange rates for the day. Strike did not fall outside of that range on either day. It is easy to believe that the real-world exchange rate at the time of the conversion was indeed close to or the same as the exchange rate that Strike applied to the conversion.

I speculate that in an effort to be fair to its customers, for automated conversions like this, Strike may use some moving average of recent transaction exchange rates across some number of exchanges to arrive at a specific exchange rate for use in the particular payroll-related conversion. To say this differently, I speculate that what Strike would not do is simply match up the payroll direct-deposit customer’s offer with only some single would-be counterparty (that might be an outlying data point).

Summary. From the various Internet discussion groups, one learns of several types of disappointment that a bitcoin buyer might encounter — fees for bringing money into an exchange, disappointingly bad exchange rates, disappointingly large fees for the conversion process, or disappointingly large fees for the “transfer out” to a cold wallet. I have not seen any of these disappointments with this payroll direct-deposit process at Strike.

Leave a Reply